Uncertainty about tariff policies overshadows strong jobs, auto sales numbers

Sentiment sours as businesses and consumers brace for fallout

With far-reaching tariffs rolling out and additional levies being announced unpredictably, American businesses and consumers are bracing for impact. The broad-based equity market selloff of the past week marked the culmination of months of souring sentiment, which a wide range of surveys confirms.

Even seemingly strong readings of economic activity, such as a surprisingly hot report that recorded 228,000 new jobs in March, felt outdated after President Donald Trump's declaration of sweeping tariffs on April 2. The strength of that number is likely to complicate the Federal Reserve's near-term ability to lower rates, given policymakers reliance on employment and inflation data to drive their decisions.

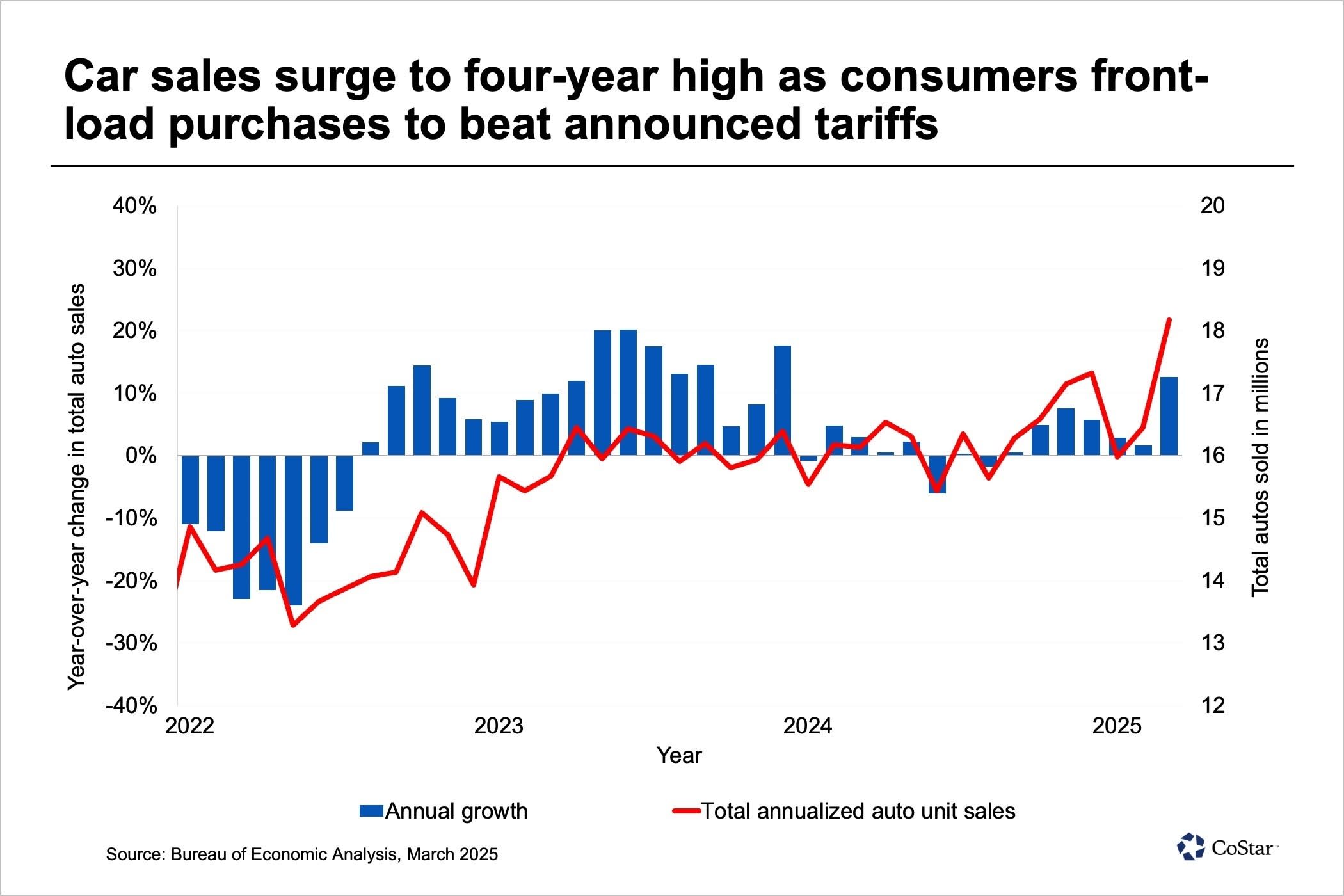

A higher-than-expected jump in auto sales in March also had to be taken with a grain of salt, given it likely reflected front-loading to avoid the impacts of looming import taxes rather than organic growth. The buying spurt could presage slower sales later in the year. About 18.2 million light- and heavy-duty vehicles were sold on an annualized basis in March, according to the U.S. Bureau of Economic Analysis, the highest total since the economy reopened in the spring of 2021.

Although improved weather in March may have accounted for some of the 12.6% year-over-year increase, the largest jump came in sales of foreign cars and light trucks, such as pickups and SUVs, which increased by nearly 18%. Aside from a handful of months during the post-COVID reopening, the total number of 4.2 million foreign units sold was the highest since 1987.

A 25% tariff on imported motor vehicles went into effect on April 3, with exemptions for parts made in Canada and Mexico and covered under a U.S.-Mexico-Canada trade agreement. Additional tariffs on major auto parts are scheduled to go into effect in May. The full suite of tariffs, if USMCA exemptions remain in place, will add up to 5% to the consumer price of vehicles, Oxford Economics estimates.

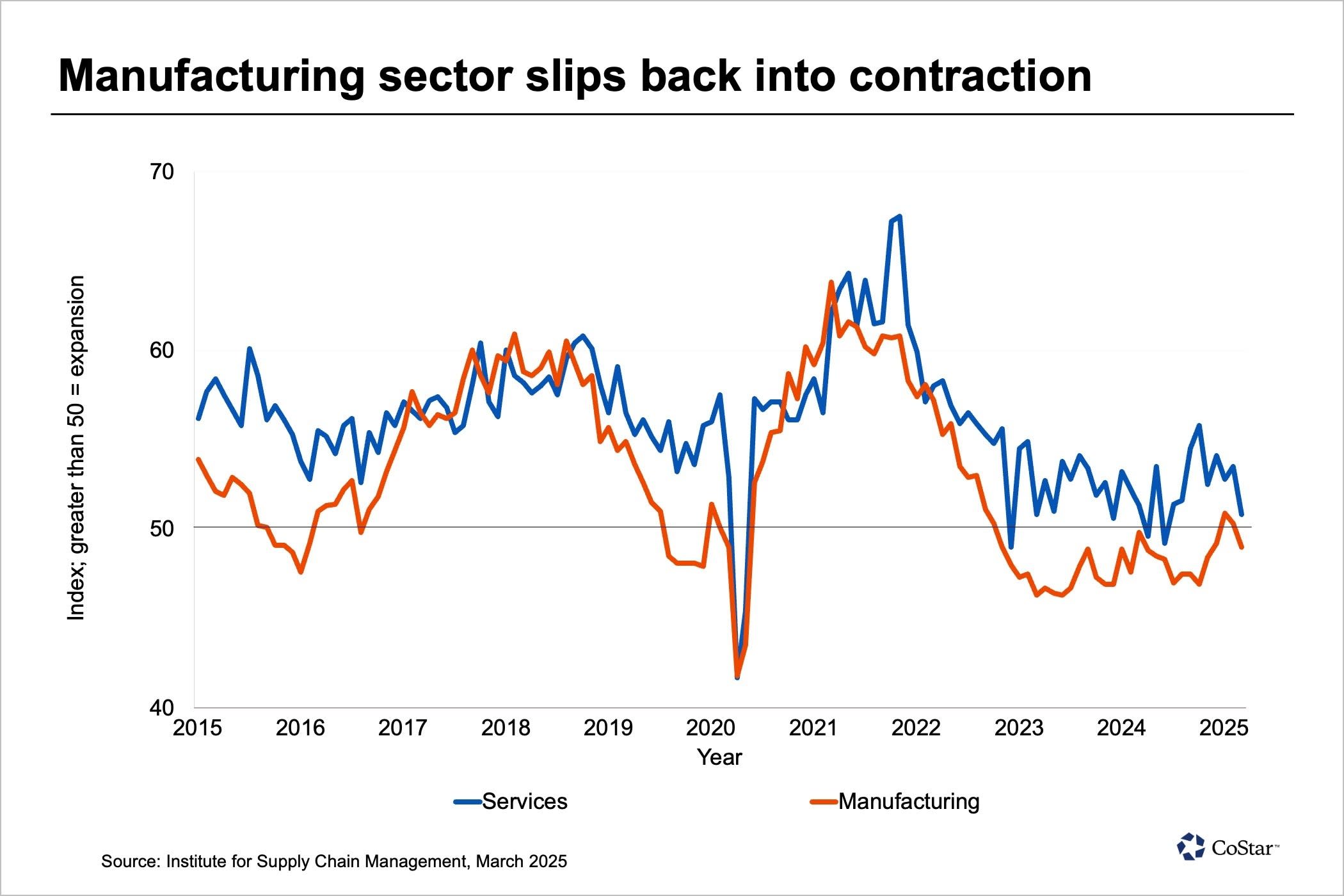

Stockpiling wasn’t limited to the automotive sector. Tariff concerns sent the manufacturing sector back into contractionary territory at 49% after two months of expansion, according to the Institute for Supply Management’s monthly survey of purchasing managers. And though the services sector remained in expansion, that index fell 2.8 percentage points to 50.8%, its lowest level since June 2024, as new orders slowed and the share of service businesses expecting to add workers fell nearly six percentage points.

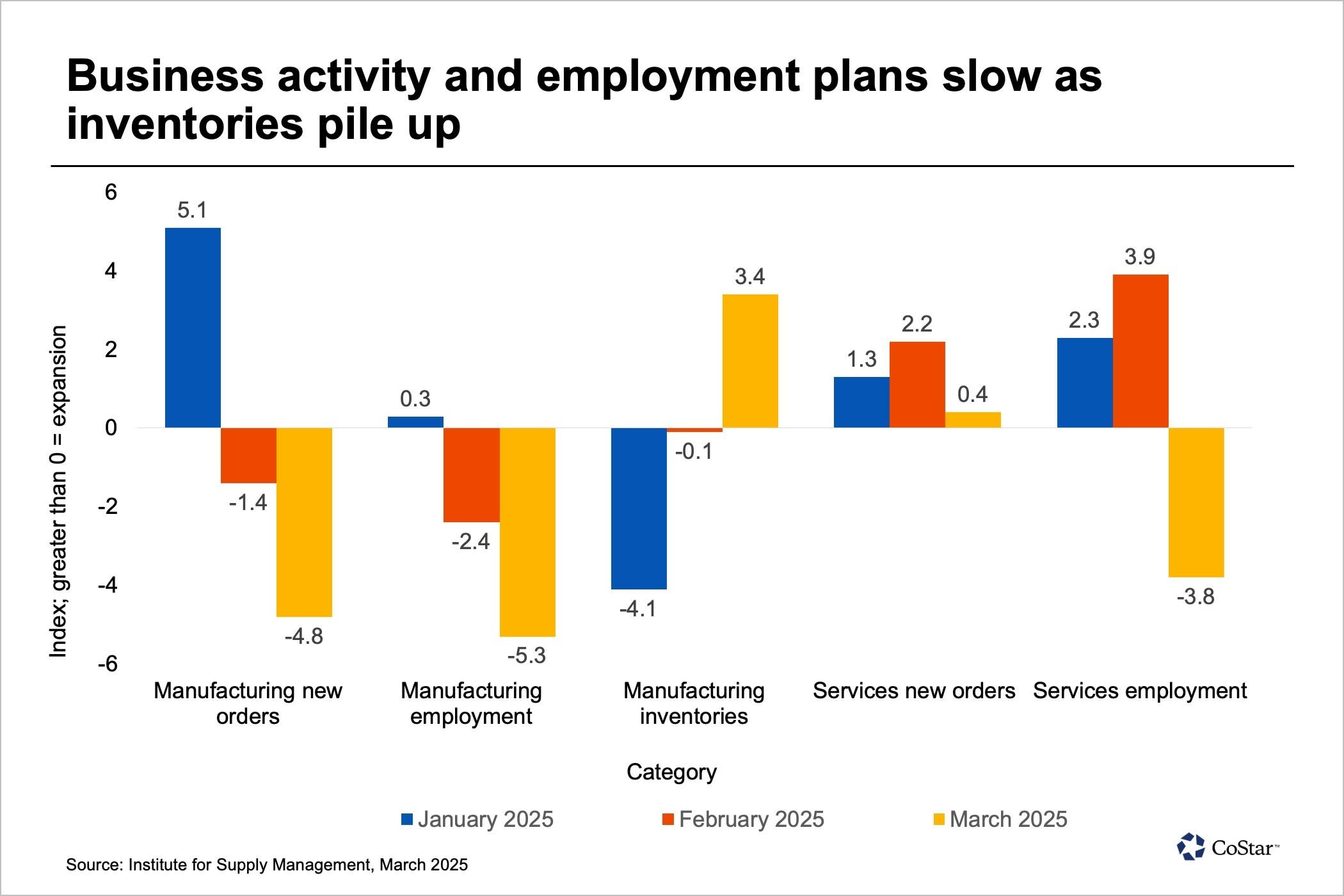

The manufacturing index would have fallen lower if not for an uptick in respondents reporting higher inventories. New orders and employment outlooks fell substantially for manufacturers, an inversion from January when new orders were increasing while inventories were declining. The share of respondents reporting higher prices rose to 46% among manufacturers while remaining elevated at nearly 29.3% for service-sector respondents.

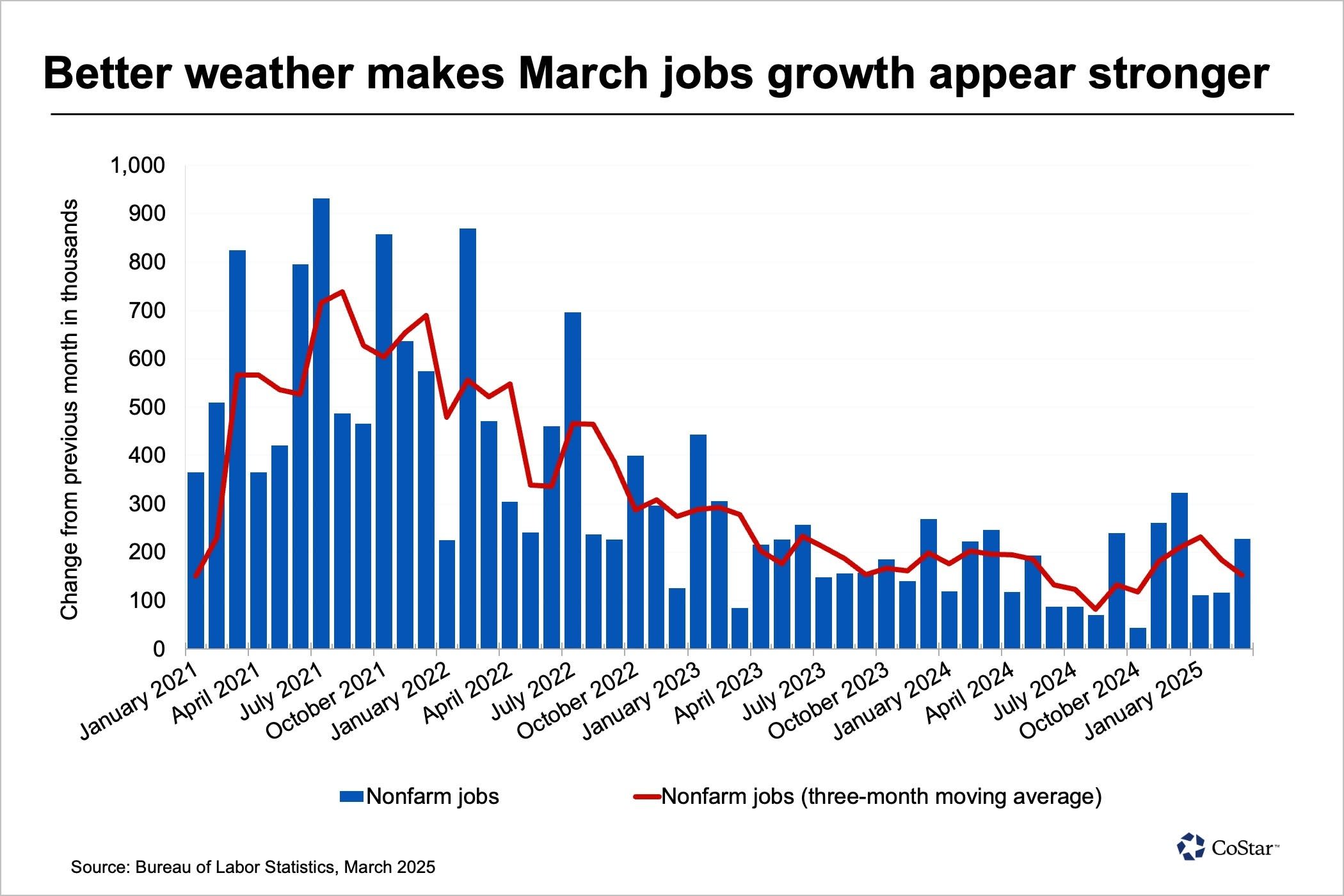

Despite the sluggish signals from the private sector in the purchasing manager’s index surveys, the March jobs report beat expectations by adding more than 228,000 jobs. The report, which reflected the conditions of the week of March 12, predated some of the more recent tariff uncertainty.

Growing demand for healthcare continued to power job growth, with one-third of job gains coming from the noncyclical healthcare and education sectors. Additionally, the end of the King Soopers grocery store chain strike in the western U.S. added 10,000 workers to payrolls, leading to a one-time uptick in retail sales. At the same time, warmer weather helped reheat restaurant hiring, which had contracted earlier in the year.

The report likely understated the impact of federal government layoffs. While the March report showed 4,000 fewer employees on federal payrolls, when added to February’s 11,000-job decline, laid-off federal workers receiving severance payments won’t be fully reflected in the jobs report until fall.

Overall, the three-month rolling average of monthly job gains was 152,000, roughly on par with the 2024 average. The seemingly solid report, combined with continued inflationary pressure revealed in the Purchasing Managers' Index surveys and other forecasts, complicates the Federal Reserve’s prospects of lowering short-term interest rates as the central bank seeks to uphold its mandate of maximum employment and stable inflation.

While tariff expectations have driven inflationary purchasing, the resultant stockpiling could result in lower demand in the coming months. Combined with a continued equity selloff, further demand destruction and subsequent negative impacts on economic growth become an increasing possibility if policy uncertainty persists.

What we’re watching

The administration reported that 50 nations have reached out to discuss the tariffs targeting their exports to the U.S., no doubt hoping for some relief from the historic rates announced so far.

The chaotic nature of the decision-making and the administration's general recalcitrance to reconsider its posture so far have only made worries more widespread. Adding to the uncertainty remains the possibility that negotiations will yield more balanced and targeted tariffs, after which markets may breathe a sigh of relief.

Additional Info

Media Contact : https://www.costar.com/

Related Links : https://www.costar.com/

Source : https://www.costar.com/