Store openings overtake closings as retail leasing normalizes

Fewer bankruptcies temper shutdowns

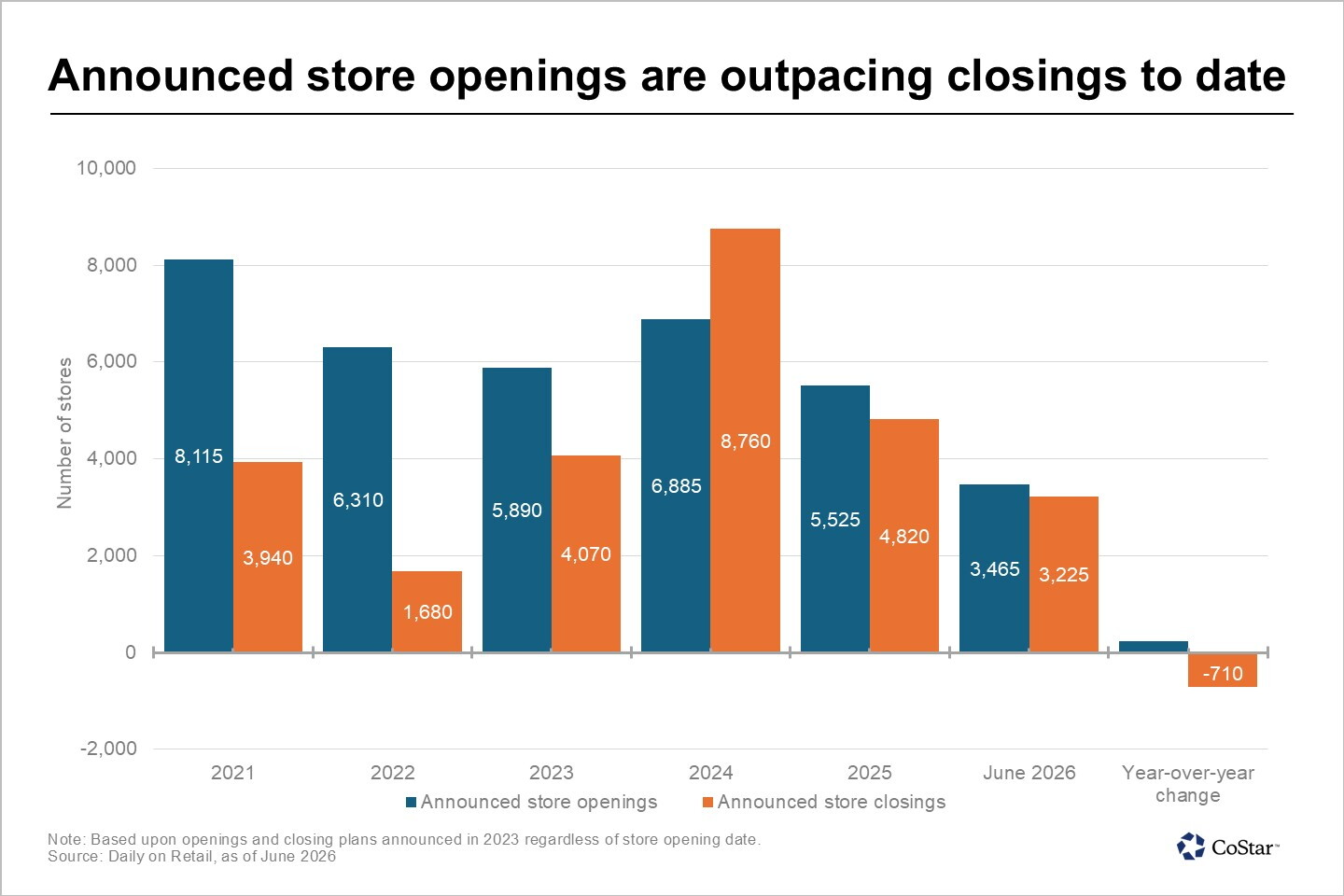

After a wave of store closings in 2025, activity has normalized in 2026 as new stores modestly outpace shutdowns so far this year.

The shift reflects fewer large-scale retailer bankruptcies and demand for physical space from those in expansion mode, rather than any fundamental change in conditions for that type of real estate.

U.S. retailers have announced plans to open approximately 3,465 stores and close roughly 3,225 locations through mid-June, according to online retail store-tracking service Daily on Retail. For the same time last year, the number of announced store closings, at 3,935, exceeded openings, at 3,230. The reduction in closings is mainly driven by fewer distressed retailer shutdowns.

In 2025, a concentrated set of bankruptcies drove a disproportionate share of closings. That pipeline has since thinned, removing a key source of volatility.

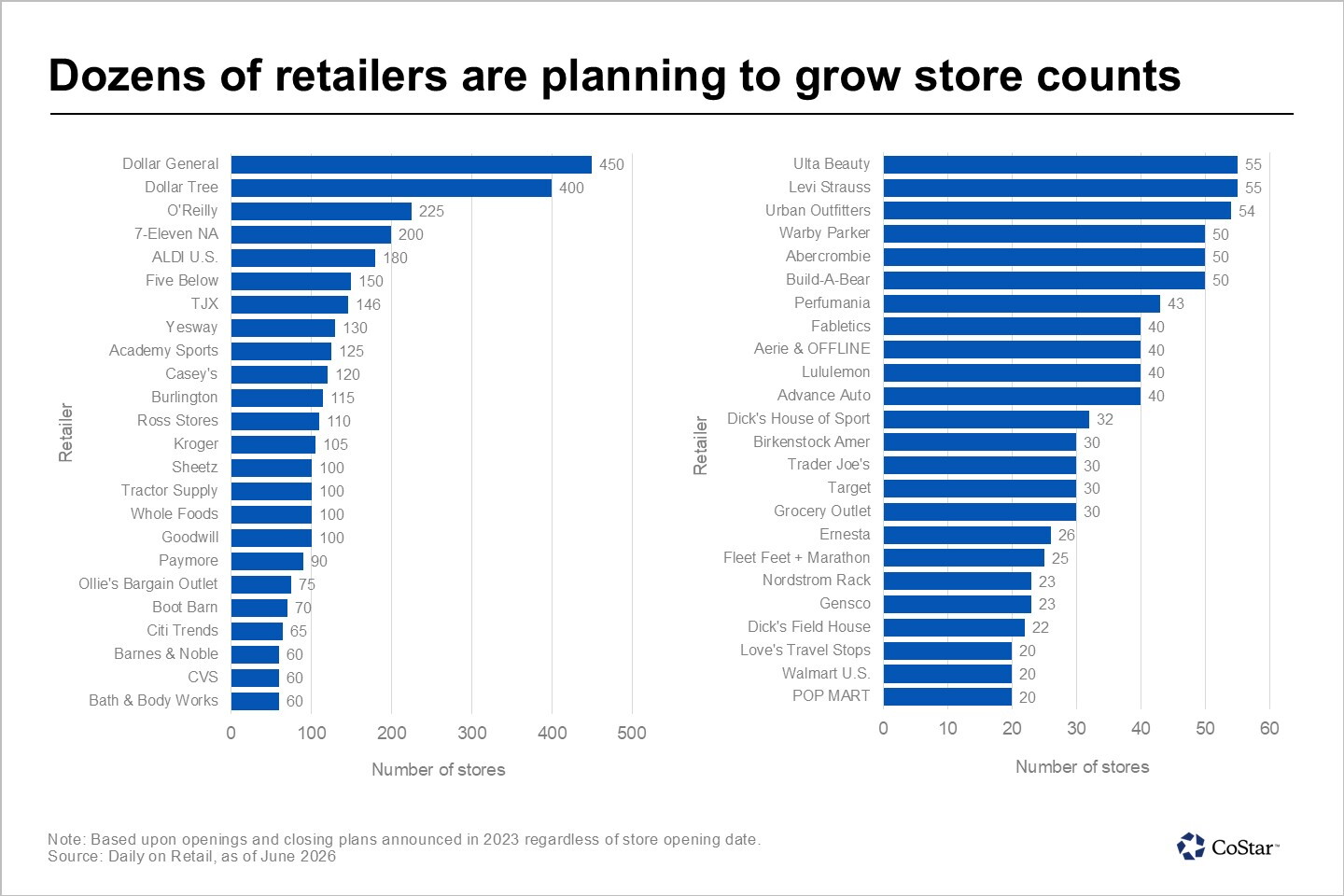

Retailer expansions remain highly concentrated among value-oriented and necessity-based retailers, which continue to capture market share as consumers are more cost-conscious.

Dollar General, with 450 planned openings, and Dollar Tree, with 400, headline the list. Other expanding chains include O’Reilly Auto Parts with 225 planned store openings, and 7-Eleven with 200. Off-price and discount chains also remain active, with aggressive store openings planned by TJX, Burlington, Ross Stores, Five Below, and Ollie’s Bargain Outlet.

Grocery and essential retail operators are similarly active. Discount supermarket chain Aldi continues to expand its property, while Kroger, Tractor Supply and Whole Foods Market are pursuing incremental store growth tied to population shifts and share gains.

This concentration of store openings in value, grocery, and necessity retail is consistent with broader performance trends, in which these segments have continued to outperform discretionary categories in both traffic and sales.

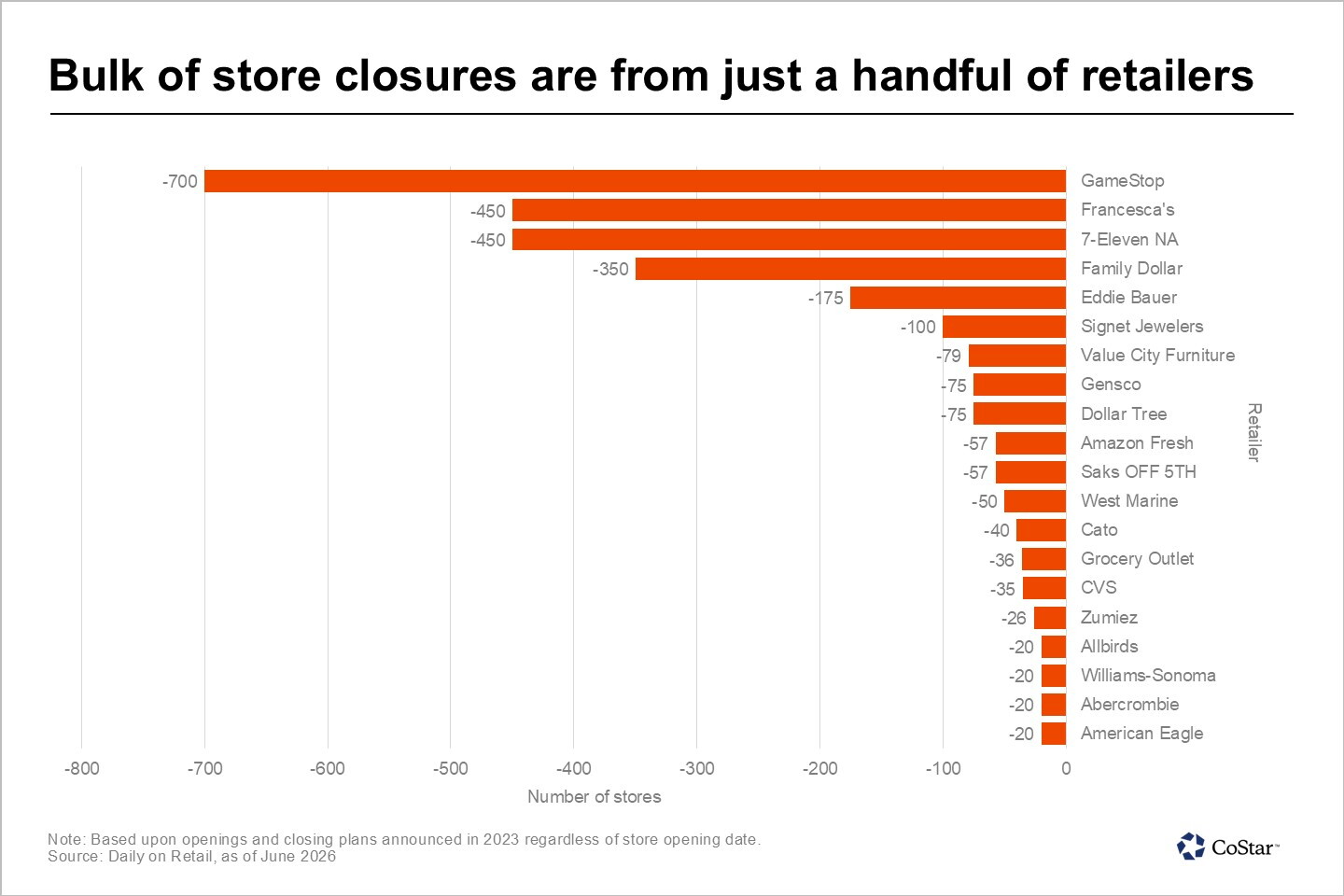

Store closings, while still elevated in certain retail segments, is more fragmented and increasingly tied to portfolio optimization rather than broad-based distress.

GameStop, with 700 planned closings; 7-Eleven, with 645; women's fashion apparel retailer Francesca’s, with 450; and Family Dollar, with 350, account for a meaningful share of the announced reductions.

Excluding Francesca’s, each represents legacy footprint rationalizations rather than liquidation-driven events, largely due to retailers' decisions to exit underperforming locations and improve overall store productivity.

This trend of more retailers seeking to rationalize their store footprints rather than close locations in liquidation-driven events has become a defining characteristic of the current environment as more retailers simultaneously open and close stores. This is evident across multiple sectors and reflects a more normalized operating environment.

7-Eleven provides a clear example, as it plans to close hundreds of older, lower-performing locations while investing in new formats focused on prepared food and higher sales throughput.

Similar strategies are being employed across the apparel, specialty, and grocery sectors, where retailers are reallocating capital toward stronger markets, resizing store footprints, and adapting formats to evolving consumer behavior.

Digitally native brands and specialty retailers are also selectively expanding, reinforcing the concept of brick-and-mortar stores as a core component of omnichannel strategies.

Wayfair’s planned eighth large-format store and expansion from emerging concepts underscore how physical locations are increasingly being used to drive brand awareness, improve fulfillment economics, and support customer acquisition. These store openings tend to be targeted and market-specific, rather than broad-based, but remain an incremental source of demand for retail space.

From a real estate perspective, the net balance between store openings and closings is increasingly secondary to the churn itself. Vacated retail space is being absorbed at a steady pace by expanding tenants, particularly in value and service-oriented categories, preventing any sustained rise in availability.

The result is a retail real estate market defined less by contraction or expansion and more by continuous portfolio optimization, where retailers refine footprints in response to shifting demographics, operating costs and evolving demand patterns.

Additional Info

Media Contact : costar.com

Related Links : costar.com

Source : costar.com